This post examines the feasibility of success for Canary Fly, which commences operations between Gran Canaria and Tenerife on November 15th 2013 and also for a new airline (Islas Afortunadas Air) which proposes operating on this same route, starting early in 2014.

Background

Tenerife (TF) and Gran Canaria (GC) easily have the two largest populations of the Canary Islands at 910,000 and 860,000 respectively in 2012. In addition, Tenerife had almost 100,000 tourists on the island on any given day whilst for Gran Canaria, the equivalent figure was 73,000. The overall resident and tourist population of the two islands is therefore just shy of 2 million people.

The transport market between the Canary Islands’ two main islands can best be described as cut-throat. There are three major players in the market, namely Fred Olsen Ferries, Armas Ferries and Binter operating inter-island air services.

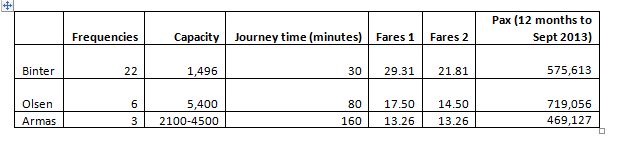

Figure 1: Characteristics of the main players in the Tenerife-Gran Canaria Travel Market

In figure 1, the frequencies are shown for weekdays, each way. Binter’s aircraft operate with 68 seats and the Fred Olsen vessels have capacity for roughly 900 each. Armas does not state which vessels are used on the TF-GC route, so the capacity figures are an estimate.

The two fares columns are those applying to residents who enjoy a 50% discount. Fares 1 shows prices available for travel in the following week (the enquiry was undertaken on Saturday, 2nd November 2013) and Fares2 shows the cheapest fares widely available in January-March 2014.

Olsen operates from the port of Agaete in Gran Canaria. Although this port is some distance from the city of Las Palmas (a similar distance between the airport and the city), the company provides a free bus link. At Santa Cruz de Tenerife, the port is close to the city centre whilst the airport, Los Rodeos, is some 7km further away from the city centre; Binter services do operate to Reina Sofia airport (TFS) but only with one return flight per day.

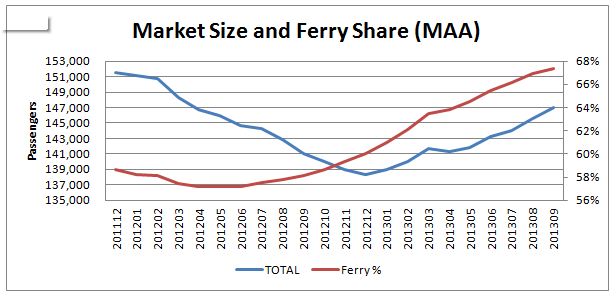

Figure 2 shows the evolution of the market from the end of 2011 to September 2013.

Figure 2: Total Market Size of GC-TF Travel Market

It is clear from this figure that whilst the overall market declined in 2012, it has shown strong growth in 2013. It is also evident that this growth has been attributable almost entirely to ferry traffic, which has shown a steady increase in market share from mid 2012 (57% to 67% in the 12 months to September 2013).

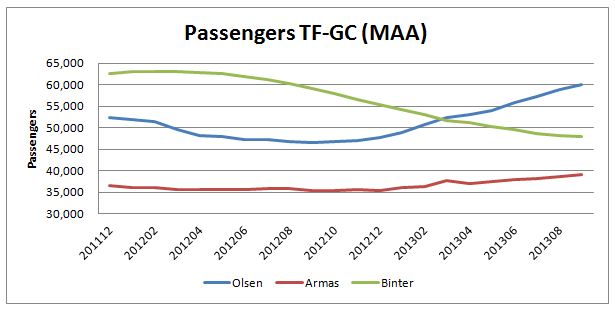

This is confirmed in figure 3 below which has shown Binter to be in decline since spring 2012. Olsen’s passenger volume has increased significantly over the same period, whilst Armas has exhibited rather smaller increases over the same period.

Figure 3: Split by Operator of the TF-GC Travel Market

How has Binter reacted to the reduction in demand? Broadly speaking, it has cut flights to maintain load factor within the range 55-60% (see figure 4).

Figure 4: Binter’s Demand and Load Factor on the TF-GC Route

In 2011, Binter (plus the smaller competitors) operated just over 1,600 one way flights per month on average between the two islands. By September 2013, this figure had declined to 1,215, a decrease of 25%. By contrast, Binter (including its affiliates) was achieving a load factor in excess of 70% over all its routes out of Gran Canaria, the airline’ main hub, during the first nine months of 2013.

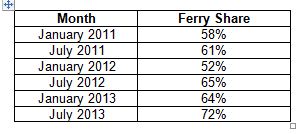

And how have the ferries achieved this strong growth in market share? In mid-2012, both companies started offering long-term promotional prices on all their routes, including their flagship GC-TF routes. Figure 5 below shows a snapshot in monthly market share which is a fair representation of what has happened before and after mid-2012.

Figure 5: Selected Ferry Market Shares

So this brings us to the major question of this post: is there room for new airlines on this route?

Market size

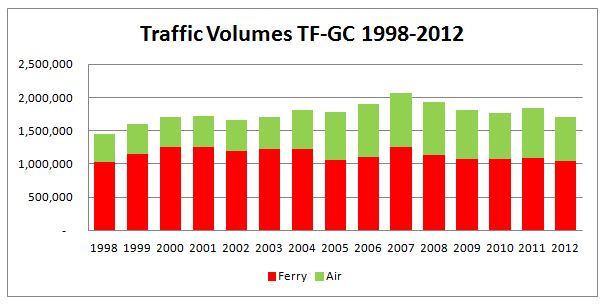

The peak year for traffic on this route between 1998 and the present was in 2007, when just over 2,000,000 passengers were carried on all routes and modes – see figure 6.

Figure 6: TF-GC Market Size 1998-2012

It is important to bear in mind, however, that the peak volume occurred at a time when the overall economy of the Canary Islands was much healthier than at present. In the third quarter of 2007, for example, the unemployment rate was reported as a little under 11%; six years later (July – September 2013) the rate had climbed to over 35%. Higher unemployment reduces disposable income and hence the propensity to travel.

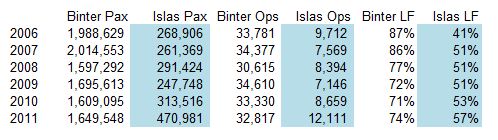

Figure 7 shows volumes and load factors at GC airport for the market leader, Binter/Naysa and the second largest airline, Islas Airways, which went bankrupt in 2012.

Figure 7: Binter and Islas Airways at Las Palmas Airport

Although Islas’ market share steadily increased during the period to 22% of demand and 27% of operations by 2011, this was never enough to overcome the hurdle of having a significantly lower load factor. Indeed, Islas never made a profit during its existence, leading to its bankruptcy in 2012. So, whilst Islas Airways MAY have expanded the overall TF-GC travel market during its existence, it was unable to do so profitably.

Price

Historical prices are almost impossible to find but anecdotal evidence suggests that Islas offered cheaper fares than its larger rival.

Quality of Service

For a 30 minute flight, the main features required of a new entrant to differentiate itself from the incumbent are frequency, ease of booking (website quality) and price. However, as we saw in figure 2, Binter has effectively saturated the market with two departures per hour for much if the day and with fares not greatly higher than Olsen (in terms of journey time, Armas does not compete with air traffic).

Capacity

Binter is operating at a relatively low load factor on its GC-TF route, below 60%. What this means in effect is that Binter has the potential to flood the market with cheap tickets to fill these empty seats (roughly 27 per aircraft per flight, on average) and make life for a new entrant very difficult indeed.

Market Opportunity or Commercial Suicide?

As the incumbent, Binter has the power to destroy competitors, as we have seen in the case of Islas Airways. Coupled with the fact that the ferries, in particular Fred Olsen, is now the dominant carrier on the GC-TF route and is thus the price leader in the market, it will be extremely difficult for a new air carrier to develop a profitable business in this market.